Unlocking activity: how quickly will the European economy emerge?

The COVID-19 pandemic and the containment measures it has necessitated have profoundly disrupted people’s lives and the economy. Global demand, supply chains, labour supply, industrial output, commodity prices, foreign trade and capital flows have all been affected. The pandemic struck the European economy when it was on a moderate path and still vulnerable to new shocks. It has also snuffed out nascent hopes that a trough might have been reached when manufacturing activity and foreign trade showed signs of bottoming out at the start of this year. Given the severity of this unprecedented worldwide shock, it is now quite clear that the EU has entered the deepest economic recession in its history.

Real-time data suggest that economic activity in Europe has dropped at an unusually fast speed over the last few weeks, as the containment measures triggered in response to the crisis by most Member States in mid-March have put the economy into a state of hibernation. Economic output is thus set to collapse in the first half of 2020 with most of the contraction taking place in the second quarter. It is then expected to pick up, assuming (i) that containment measures will be gradually lifted, (ii) that after these measures are loosened the pandemic remains under control, and (iii) that the unprecedented monetary and fiscal measures implemented by Member States and the EU are effective at cushioning the immediate economic impact of the crisis as well as at limiting permanent damage to the economic tissue.

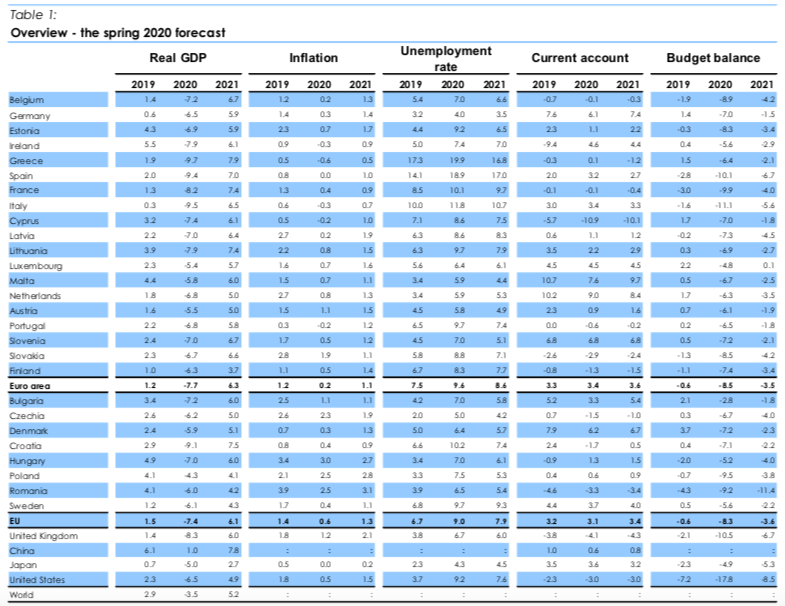

Under these benign assumptions, EU GDP is forecast to contract by about 71⁄2% this year, far deeper than during the Global Financial crisis in 2009, and to rebound by only 6% in 2021. This rebound, however, would leave the European economy, at the end of this forecast horizon, about 3% lower than the output level implied by the autumn forecast. The same holds for the volume of investment that is forecast to be about 7% lower than expected in the autumn. Next year, the number of employed people in the EU would be, on average, about 1% below what was recorded in 2019. Lower employment and investment reduce potential output, whereas the record-high uncertainty about jobs, incomes and sales, are set to hold back demand for some time. This suggests an only gradual (‘U-shaped’) recovery. Uncertainty about the pandemic remains huge, and different assumptions than the ones underpinning the baseline scenario analysis on which this forecast is anchored would lead to very different projections.

The COVID-19 crisis is a symmetric shock hurting all Members States. Their strong economic interconnectedness is magnifying the aggregate demand and supply shocks. While the recovery looks set to be incomplete in almost all countries, the impact of the crisis and the way Member States will emerge from it is set to be uneven. How well countries emerge will depend not only on the severity of the pandemic and the stringency of their containment measures, but also on their specific economic exposures and initial conditions, and the discretionary policy responses that their levels of policy space allowed them to afford. Due to their strong interdependencies, an incomplete recovery in one country would spill over to all the other countries and dampen economic growth everywhere.

As the COVID-19 virus spread around the world, many governments were forced to take extreme precautionary public health measures to save lives and prevent health care systems from being overwhelmed. These measures made it impossible for economic life to continue normally, effectively shut down large portions of the economy and derailed the incipient bottoming out in the global economy that had started to emerge around the turn of the year. This crisis has also triggered a collapse in oil and many other commodity prices and sparked financial turmoil. This has been particularly damaging for commodity exporting countries as well as emerging economies with high US dollar-denominated debt. The combination of these three shocks is expected to push the global economy into a deep recession in the first half of 2020. The massive health and macroeconomic policy efforts taken across most major economies are, however, assumed to contain the pandemic and to limit its negative impact on the global economy to a deep but essentially temporary downturn. Overall, global GDP (excluding the EU) is projected to contract by about 3% this year, which is a sharper downturn than during the Global Financial Crisis in 2008-2009. It is then expected to rebound by 5% in 2021, implying that global output should recover above it 2019 level but remain well below the level projected in the autumn 2019 forecast.

Both advanced economies and emerging markets are expected to be in recession this year, but the restart in economic activity is set to be gradual and uneven across countries and regions. In most advanced economies outside the EU, the rebound is forecast to be insufficient to bring output back to their pre-pandemic levels by the end of the forecast horizon. Growth dynamics are expected to ‘normalise’ in China, while only a limited pick-up is set to take hold in Latin America, the Middle East and Africa. For many emerging and low-income countries with limited capacity to deal with a health crisis of this magnitude as well as limited policy space to absorb the macroeconomic impact, the economic shock is projected to be more persistent, as it is also compounded by subdued prospects for commodity prices and tightened financial conditions.

After falling into near stagnation last year amid elevated trade policy uncertainty, world import volumes (excluding the EU) are likely to fall by more than 10% this year due to an unprecedented collapse in international trade concomitant to the lockdown measures taken across the globe in the first half of the year. As these measures are assumed to be gradually lifted and global demand recovers, trade in goods is expected to start rebounding in the second half, while trade in services, particularly tourism, is set to rebound more slowly. Next year, non-EU world imports are set to increase by about 63⁄4%, a pace closer to global economic activity. A stronger rebound is unlikely, as trade policy uncertainty is assumed to remain unabated and the pandemic crisis is expected to trigger some permanent damage to global value chains.

The COVID-19 shock has reverberated across global financial markets as the spread of the virus outside China led to a sudden repricing of risks in March while safe haven sovereign yields declined. In Europe, riskier market segments such as equities and high-yield corporate bonds took a hit once it became clear that COVID-19 was also strongly affecting the continent. This resulted in the fastest market sell-off since the Global Financial crisis of 2008-2009, reflecting the rapid and sharp deterioration of the economic outlook and profitability prospects, but also by the severe liquidity dry-up that non-financial corporations (NFCs) were confronted with. In the euro area sovereign markets, a divide re-emerged between the core and the periphery,suggesting renewed investor concerns about debt sustainability, in particular in case of insufficiently coordinated support at the EU level.

The monetary and fiscal policy response to the crisis, both globally and in the EU, has been swift and strong with unprecedented measures taken to contain the macroeconomic fallout and alleviate liquidity pressures. In the EU, policy announcements contributed to the stabilisation of financial markets with spreads narrowing for corporates and sovereigns and equity markets recovering part of their losses in April, although markets also benefited from reports suggesting that the pandemic might have peaked in some countries. In the euro area, the ECB began in mid-March to take a broad range of monetary and credit policy measures. A particular aim was to ensure (bank) credit flows to NFCs so as to prevent temporary liquidity shortages from evolving into solvency crises. The Pandemic Emergency Purchase Programme (PEPP) announced by the ECB aims to prevent the fragmentation of credit markets and the impairment of monetary policy transmission. In response to these liquidity constraints, EU Member States have also implemented a number of liquidity support measures, such as partial or total guarantees on bank loans. These liquidity measures amount to 22% of EU GDP and were complemented by existing EU budget instruments offering support of up to about 41⁄2% of EU GDP.

Lending support from the banking sector will be vital, not only during the crisis, but also during the economic recovery. But banks are particularly exposed to the economic recession as more borrowers are likely to default and because the prices of securities on their balance sheets have taken a beating. The underperformance of their share prices since late February is a reflection of such concerns. However, as European banks have strengthened their capital positions very substantially over the last 10 years, they should be resilient enough to withstand even a massive economic recession. Overall, it is assumed that the wide range of policy measures will be largely effective at protecting the corporate sector from widespread bankruptcies this year and lending flows are expected to grow again next year when the economic recovery gains traction.

All demand components will be hit hard by the pandemic except government consumption and public investment, which are playing a stabilising role. Private consumption, which for several years has been the backbone of economic growth in Europe, is expected to contract by about 9% in both the EU and the euro area this year. This sharp fall is, however, forecast to be mainly concentrated in the current quarter, as the lack of opportunity to spend results in ‘forced savings’. It is then expected to start recovering quickly once containment measures are lifted. But the recovery is set to be incomplete, as spending on travel and recreational services will lag behind because restrictions affecting these activities may last longer and because the fiscal measures implemented to protect employment and workers’ incomes will only limit rather than prevent a drop in household purchasing power this year. Moreover, uncertainty about employment and income prospects will likely ensure that precautionary savings remain higher than they were before the crisis well after the lockdowns have ended.

Business investment is likely to take a very severe double-digit hit this year, as many businesses, including the already fragile investment-intensive car industry, are experiencing a series of incremental supply, demand and financial shocks. Faced with heightened uncertainty about future sales prospects, firms are likely to postpone or even cancel their investment plans. Moreover, the lack of revenue during the lockdowns may constrain their ability to finance investment projects in the near term, or even longer if the increase in debt triggers a need to deleverage. The economic fallout is also expected to lead to a sharp fall in capacity utilisation, reducing the need for investment linked to capacity expansion and lowering incentives for upgrading the capital stock. Once the adverse impact of the COVID-19 pandemic abates, investment should find support from a highly accommodative monetary policy, lower uncertainty and some recovery in profits. The expected rebound of euro area and EU investment by slightly more than 10% next year, however, should only help to recover some of the lost ground. Compared to the levels projected in the autumn 2019 forecast, the cumulated shortfall in investment in the EU is expected to amount to almost EUR 850 billion at current prices, or 6% of EU GDP.

Euro area exporters already suffered last year from weakening foreign demand largely reflecting trade tensions and elevated trade policy uncertainty. Since the pandemic, the halt in the free movement of people, goods and services is set to result in a sudden, severe and synchronised drop in external demand. The euro area is expected to be particularly affected due to its relatively high participation in global and intra-EU value chains. Euro area exports are thus forecast to fall by about 13% in 2020 before rebounding incompletely by close to 10% in 2021. A stronger catch-up is unlikely due to enduring weakness of foreign demand, likely delays to the resumption of production and supply chain normalisation, as well as still elevated levels of uncertainty. As exports and imports are expected to move almost in parallel, the contribution of net exports to GDP growth in the euro area and the EU should be relatively small this year and next.

The COVID-19 pandemic and the confinement measures it has necessitated have led to significant disruptions and completely changed the prospects of European labour markets that were, up to early 2020, the bright spot in the expansion years. National policy measures, such as short-time work schemes for workers, wage subsidies for the self-employed as well as liquidity measures for firms have been taken to limit employment losses during the confinement period and to ensure that work can resume smoothly once restrictions can be relaxed. Assuming that these measures are effective, the fall in employment this year is expected to be contained, particularly in terms of headcount given the sharp drop in working hours. Nevertheless, some persistent negative impact (hysteresis) is likely, in particular for the more precarious workers who have often been the first to lose their jobs and young cohorts unable to find their first job. The euro area unemployment rate is expected to increase from 7.5% last year, its lowest level in more than a decade, to about 91⁄2% this year and to decrease next year while remaining well above its pre-pandemic level in 2021. Unemployment rates are expected to rise very differently across the EU, not only because of the size and effectiveness of policy measures, but because of pre-existing vulnerabilities (e.g. high share of temporary contracts) and different sector specialisations (e.g. tourism).

Overall, the pandemic is likely to put downward pressure on prices because the effect of lower demand will outweigh price increases sparked by supply chain disruptions. This has already been signalled by recent developments in euro area inflation. However, in March headline HICP inflation has also been sunk by the steep fall in energy prices. The combination of weakening economic activity, which makes the pass-through from wages to prices even more difficult for firms, and a deteriorating labour market outlook limiting future wage increases, translates into lower domestic price pressures that are set to weigh on core inflation going forward. Combined with markedly lower oil price assumptions, the forecast for HICP inflation in the euro area has been significantly revised down to 0.2% this year. It is forecast to increase to 1.1% in 2021, largely on the back of positive base effects in energy prices.

The aggregate general government deficit is expected to surge from 0.6% of GDP in 2019 to 81⁄2% of GDP in both the euro area and the EU this year. This sharp increase largely reflects the work of automatic stabilisers and sizeable discretionary fiscal measures. In 2021, the headline deficit is forecast to decrease to 31⁄2% of GDP in both areas due to the expected rebound in economic activity and the unwinding of most of the temporary measures adopted in response to the COVID-19 crisis. After having been on a declining trend since its peak in 2014, the euro area’s aggregate debt-to-GDP ratio is projected to reach a new peak of close to 103% in 2020 before decreasing by about 4 pps. in 2021 based on a no-policy-change assumption.

The fiscal stance for the euro area is expected to be very expansionary in 2020 given the discretionary measures related to the COVID-19 outbreak, while most of these discretionary measures taken are set to be discontinued next year under a no-policy-change assumption. In several Member States, even those particularly affected by the pandemic, the limited availability of fiscal space implies a more muted policy response than elsewhere. Given the economic disruptions caused by the coronavirus outbreak, the ECB’s subsequent broad range of easing measures, and only a very limited increase in long-term inflation expectations, real short and long-term interest rates should remain clearly in negative territory over the forecast horizon.

Risks to this forecast are extraordinarily large and concentrated on the downside. The pandemic could become more severe and last much longer than assumed, requiring more stringent and longer lasting containment measures than assumed in this baseline scenario. This would result in much worse outcomes as shown by the scenario analysis presented in this document. This would also be the case in a scenario where a second wave of infections take place later this year.

As some of the Member States hit hardest by the virus are also those with the least policy space to respond, divergences across countries could become entrenched if national policy responses are not sufficiently coordinated or if there is no strong common response at the EU level. This could distort the internal market and ultimately threaten the stability of the euro area.

Globally, the pandemic period could also trigger more drastic and permanent changes in attitudes towards global value chains and international cooperation that would particularly hit open economies such as the EU. Inside the EU, the pandemic could also leave permanent scars, such as a large number of bankruptcies and higher hysteresis effects in the labour market, that are not taken into account in the baseline scenario.

The risk also remains that new tariffs might be applied, which could adversely affect business investment plans. Moreover, reaching the end of the transition period foreseen in the Withdrawal Agreement between the EU and the UK will dampen economic growth, even if a free trade agreement between the EU and the UK is concluded. This will affect particularly the UK, but also the EU, albeit to a lesser extent.